LIC Jeevan Labh Policy 2023

what is LIC Jeevan Labh policy?

Being a leading insurance provider in India, LIC policies are a popular choice for customers when it comes to buying insurance cover. With a very wide range of policies offered by LIC, LIC Jeevan Labh offered by LIC of India is one of the most LIC Jeevan Labh Insurance is the best selling endowment insurance plan Comes with many benefits for the buyers .

LIC’s superhit policy! Will have to invest only Rs 7,572, will get a return of Rs 54 lakh

he Life Insurance Corporation of India (LIC) offers a variety of helpful programmes to its clients. wherever there is a policy that applies to all ages. The LIC Jeevan Labh insurance is one of them.

The advantages of safety and savings are both provided by LIC Jeevan Labh. By making an investment in this plan, you will get a lump sum payment when it matures. You will simply need to set aside Rs 7,572 each month for this policy. You can also include Rs. 54 lakh for your future. This plan has restricted premium payments and is not connected.

If the policyholder passes away, it offers the family financial support. Additionally, the insured will receive a significant sum of money if he lives till maturity. Investors in this plan are free to select the premium’s size and duration based on their preferences.

Features and Benefits LIC Jeevan Labh

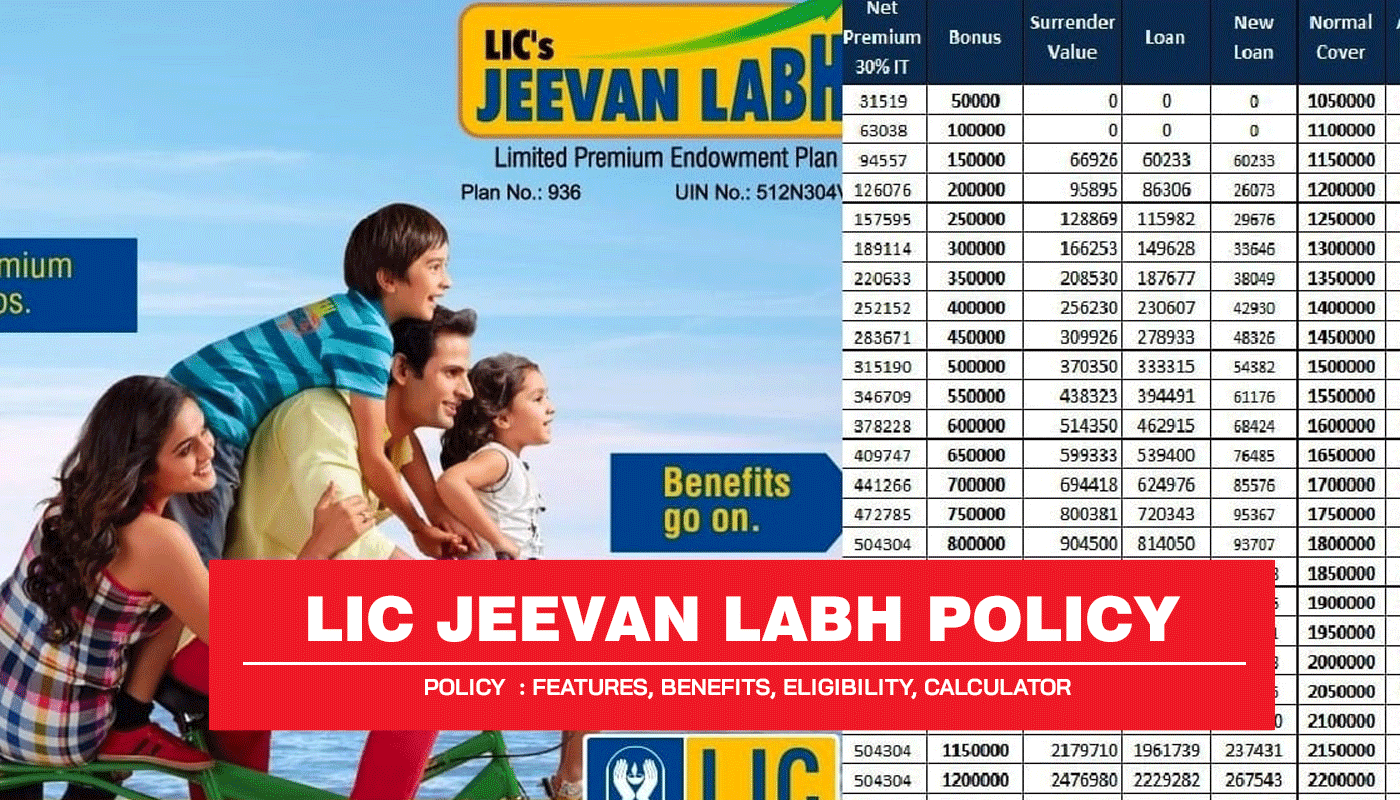

LIC Jeevan Labh is a participating, non-linked, limited premium payment life insurance policy offered by the Life Insurance Corporation of India (LIC). It provides a combination of life coverage and savings benefits. Here are the key features and benefits of LIC Jeevan Labh:

- Death Benefit:

In the event of the unfortunate demise of the insured during the policy term, the death benefit is payable to the nominee. The death benefit includes the sum assured on death, along with any applicable bonuses. The sum assured on death is higher of the basic sum assured or 10 times the annualized premium.

- Maturity Benefit:

If the insured survives till the end of the policy term, the maturity benefit is paid. The maturity benefit includes the sum assured on maturity, along with any applicable bonuses. The sum assured on maturity is equal to the basic sum assured.

- Bonus Participation:

LIC Jeevan Labh is a participating policy, which means it participates in the profits of LIC. Policyholders are eligible to receive Simple Reversionary Bonuses and Final Additional Bonus, if any, as declared by LIC. These bonuses are added to the policy’s maturity or death benefit, enhancing the overall payout.

- Limited Premium Payment:

Jeevan Labh offers the flexibility of limited premium payment. The policyholder can choose to pay premiums for a limited period, which is shorter than the policy term. Premium payment terms of 10, 15, and 16 years are available, depending on the policy variant chosen.

- Policy Term Options:

Jeevan Labh offers multiple policy term options, allowing individuals to select a term based on their financial goals and requirements. Policy terms of 16, 21, and 25 years are available.

- Loan Facility:

Jeevan Labh offers a loan facility, allowing policyholders to avail loans against the policy’s surrender value after the policy acquires a surrender value.

- Tax Benefits:

Premiums paid towards LIC Jeevan Labh are eligible for tax benefits under Section 80C of the Income Tax Act, 1961. The maturity benefit and death benefit are generally tax-exempt under Section 10(10D), subject to certain conditions.

How to Apply LIC Jeevan Labh in India

To apply for LIC Jeevan Labh in India, you can follow these steps:

- Research and Choose: Begin by researching and understanding the features, benefits, and terms of LIC Jeevan Labh. Assess whether it aligns with your insurance needs and financial goals. You can visit the LIC website or contact a LIC agent for detailed information.

- Contact LIC Agent: Get in touch with a licensed LIC agent or visit the nearest LIC branch. They will guide you through the application process, explain the policy details, and assist you in filling out the necessary forms.

- Application Form: Fill out the application form for LIC Jeevan Labh. Provide accurate personal information, contact details, and other required details as specified in the form. You may need to provide supporting documents such as address proof, identity proof, and age proof along with the application.

- Medical Examination: Depending on the sum assured and your age, a medical examination may be required. LIC will arrange for a medical examination at their designated medical center or through their empaneled doctors.

- Premium Calculation: Your LIC agent will help calculate the premium amount based on factors like age, sum assured, policy term, and premium payment term. Understand the premium payment options available and select the one that suits you best.

- Premium Payment: Pay the premium amount for LIC Jeevan Labh as per the chosen payment mode (monthly, quarterly, half-yearly, or annually). LIC provides various payment options such as online payment, bank draft, or direct debit from your bank account.

- Document Submission: Submit the completed application form along with the necessary supporting documents and premium payment receipt to the LIC agent or LIC branch office. Ensure that all documents are accurate and complete.

- Underwriting Process: LIC will review your application, medical reports (if required), and supporting documents. They will assess the risk and decide on the acceptance of your application and premium rates. This process may take some time.

- Policy Issuance: Once your application is accepted and the premium is processed, LIC will issue the Jeevan Labh policy document. Read the policy document carefully, verify the details, and keep it in a safe place.

It is advisable to consult with a licensed LIC agent who can provide personalized guidance and support throughout the application process. They will help you with the necessary paperwork, explain policy terms, and address any queries you may have.

Eligibility Criteria of LIC Jeevan Labh

The eligibility criteria for LIC Jeevan Labh may vary slightly based on the specific policy variant and the terms and conditions set by LIC. However, here are some general eligibility criteria for LIC Jeevan Labh in India:

- Minimum Entry Age: The minimum entry age for LIC Jeevan Labh is generally 8 years or above. This means the policy can be purchased for individuals who have attained the age of 8 years or older.

- Maximum Entry Age: The maximum entry age varies depending on the chosen policy term. Generally, it ranges from 59 to 62 years. This means the policy needs to be purchased before reaching the maximum entry age specified by LIC.

- Policy Term: LIC Jeevan Labh offers policy terms of 16, 21, and 25 years. The eligibility for each policy term may differ, and individuals need to meet the specific age requirements for the chosen term.

- Premium Payment Term: Jeevan Labh offers limited premium payment options, where premiums are paid for a shorter duration than the policy term. The premium payment term options available are typically 10, 15, and 16 years. The eligibility for each payment term may vary.

- Sum Assured: The sum assured is the minimum amount of coverage provided by the policy. The eligibility for different sum assured amounts may depend on factors such as the policy term, age, and individual’s financial profile.

It’s important to note that the above eligibility criteria are indicative and subject to change. The specific eligibility criteria, including age limits, policy terms, premium payment terms, and sum assured, should be confirmed with LIC or a licensed LIC agent as per the current guidelines.

What is the specialty of LIC Jeevan Labh scheme

Any citizen with a legal age between 8 and 59 may invest under this LIC programme. Insurance holders will be able to deposit money for 10, 13, and 16 years under this policy. At 16 to 25 years old, maturity money will be accessible. If a 59-year-old wants to ensure that his age does not surpass 75, he can buy a 16-year insurance coverage.

On the other hand, if the policy holder passes away during the term of the insurance for any reason, the nominee will receive the benefit. Along with the bonus from LIC, the nominee will also receive the benefit of Sum Assured. The policy’s strongest suit is taken into consideration. If the insurance hasn’t expired and all premiums have been paid, this policy will return the sum insured upon the policyholder’s passing.

Will get return of lakhs?

You must be at least 18 years old to invest in this LIC insurance, and you can invest for a maximum of 59 years. If a person purchases this coverage at age 25, he must pay a deposit of Rs 7,572 per month, or Rs 252 per day. This means that Rs 90,867 will be deposited each year. This will result in the deposit of roughly 20 lakh rupees into this policy. The policyholder would receive Rs 54 lakh after the maturity period is through. You will also profit from the reversionary bonus and final additional bonus upon maturity if you invest in this LIC programme.

LIC Jeevan Labh Riders

Five optional riders are available under the LIC Jeevan Labh Policy, and they can be accessed by the policyholder by paying an extra premium.

To extend the scope of the policy’s coverage,

riders can be added to the base plan.

- Rider for the Accidental Death and Disability Benefit

- Rider for Accidental Benefit

- Rider for Term Assurance

- Rider for Critical Illness

- Waiver of Premium Benefit

Other Details of LIC Jeevan Labh Plan

- Grace Period:

The insured is given a grace period of 15 to 30 days to pay any outstanding premiums.

- Free-look Period:

If the policyholder is dissatisfied with the terms and conditions, they have 15 days to terminate the insurance.

- policy Surrender:

If the premiums are paid for a minimum of two complete policy years, the LIC Jeevan Labh Plan obtains a surrender value. The Guaranteed Surrender Value or the Special Surrender Value, whichever is larger, will be paid to policyholders. It is based on the total amount of premiums paid, the year of surrender, and the length of the insurance.

- Paid-Up Value:

The policy becomes paid-up if the life assured stops paying premiums after doing so consistently for at least two years. Afterward, dependent on the premiums paid, the sum promised decreases.

The following is the decreased paid-up sum assured:

Sum promised on death or maturity divided by number of premiums paid and remaining premiums to be paid

FAQ – LIC Jeevan Labh

What is LIC’s Jeevan Labh plan?

What is LIC Jeevan Labh Plan? Jeevan Labh LIC Plan is a non-linked, with-profit, limited premium paying, endowment plan offered by Life Insurance Corporation of India. The plan offers a lump sum benefit along with death and maturity benefits at the end of the policy term.

Which is the best LIC plan 2023?

The name of this policy is LIC Jeevan Labh Policy Plan (LIC Jeevan Labh Policy Plan) (936). This is a non linked policy. So this policy has nothing to do with the stock market. This plan is considered best for marriage of children, education and purchase of property.

Can parents buy a LIC Jeevan Labh plan for their children?

Yes, parents can purchase the Jeevan Labh coverage for kids older than 8 years old. The child in this situation will be regarded as the life assured, and as the parent, you will be responsible for paying the plan’s premium. If the life guaranteed survives the policy duration, the maturity amount will be paid to them completely.

Which payment modes are available to pay the premium for the LIC Jeevan Labh plan?

You have two options for making regular premium payments: salary saving scheme (SSS) or the National Automated Clearing House (NACH). You can make regular payments on an annual, half-yearly, quarterly, or monthly basis.

Is it possible to discontinue my LIC Jeevan Labh plan?

If you are unhappy with the terms and conditions of the life insurance policy, you have 15 days to cancel it.

What is the condition to avail loan on my LIC Jeevan Labh plan?

Only after paying the insurance provider in full for the plan’s two-year payment can a policyholder apply for a loan. The maximum loan amount must match the percentage of the surrender value specified in the insurance document’s terms and conditions.