Best Payment Gateways for Businesses for 2024: When operating a small business, having a reliable payment method is essential. Payment gateways serve as financial tools that facilitate businesses in accepting payments via debit or credit cards. In today’s digital age, where online shopping is prevalent and cashless transactions are common, selecting a user-friendly payment gateway becomes vital for businesses to cater to both corporate and consumer markets.

To select the most suitable payment gateway for your business requirements, it’s crucial to assess factors such as cost, features, and supported payment methods. Continue reading to explore the top payment gateways tailored for businesses seeking card-based payments.

| Best Payment Gateways | Best for | Payment processing fees | Monthly or annual fees |

|---|---|---|---|

| Paypal | Simple online payments | Starts at $0.49 plus 3.49%for most online payments | None for online-only payments |

| Square | Mobile payments | 2.6% plus $0.10 for card present 2.9% plus $0.30 for online payments 3.5% plus $0.15 for keyed transactions 3.3% plus $0.30 for invoices | Starts at $0 per month |

| Payment Depot | Monthly fee only | Interchange only | $79 per month for up to $250,000 in annual payments |

| Stax Payments | Monthly subscription pricing | Low “cents per transaction” fee | $99 per month for up to $250,000 per year in payments, $199 per month for up to $500,000 in annual payments |

| CardX | Surcharge compliance | Credit offset by customer surcharges. Debit 2.91%. | Starting at $29 per month for virtual terminal or $35 per month for in-person payments. |

| Paysafe | Diverse payment methods | 0.30% + $0.10 plus interchange | $9.95 PCI compliance fee and $25 monthly fee minimum |

| U.S. Bank Merchant Services | Robust payment features | Swipe/tap/dip: 2.6% + $0.10Key-in: 3.5% + $0.15 Online: 2.9% + $0.30 | $0 to $99 per month for the first terminal, $29 per month for additional terminals |

| Stripe | Online payments | 2.9% + $0.30 | Starts at $0 per month |

| Clover | Single-location businesses | Varies based on business type | $14.95 to over $100 per month |

| Braintree | Digital wallet integrations | 2.59% + $0.49 | None |

| Adyen | Omnichannel payment solutions | $0.13 plus varying interchange |

click here –Netspend Visa Prepaid Card Review 2024

Our recommendations for best payment gateways

Best for simple online payments: Paypal

PayPal, a seasoned player in online payments, offers swift registration and seamless online payment acceptance for businesses. Its services extend to mobile and in-person transactions, along with a range of financial solutions.

For online card payments, fees typically amount to $0.49 plus 3.49%. QR code payments incur lower costs, with rates at 1.90% for transactions over $10 or 2.40% for transactions of $10 or less, plus the $0.49 fee. Standard card payments qualifying for lower rates are charged $0.49 plus 2.99%.

One of PayPal’s standout features is its absence of monthly recurring fees for most businesses. In-person transactions carry a fee of 2.70% for card-present transactions or 3.50% plus $0.15 for keyed transactions. If you’re seeking to steer clear of recurring fees, especially due to low card-processing volumes, PayPal could be an excellent choice.

What makes the best eCommerce payment gateway service?

In my research and evaluation of eCommerce payment processors, I focused on the following criteria:

Accepted payment methods: Each credit card processing solution had to support all major credit card brands as a minimum requirement.

Ease of integration: Implementing a payment solution should not require coding expertise. I looked for platforms with either a fully no-code setup or comprehensive guides for seamless integration.

Security: All listed payment processors adhere to PCI-DSS compliance standards, ensuring robust security measures for online transactions.

Checkout experience: A smooth checkout process is essential for customer satisfaction. I prioritized platforms offering an intuitive and user-friendly checkout experience.

Extra features: Additional tools such as subscription support, invoicing, payment links, and card readers can enhance functionality. I considered the availability of these extras during the evaluation.

I assessed these platforms using two approaches. For those with self-service sign-up options, I personally configured the settings and integrated the solution into a webpage on my site. For platforms requiring sales interaction, I initiated communication to set up a test environment and evaluate the functionality firsthand.

Best online credit card processing system for first-time users

Pros of PayPal:

- Trusted and well-known brand may increase customer confidence and willingness to make purchases.

- User-friendly interface for both merchants and customers.

Cons of PayPal:

- Confusing pricing structure can make it difficult to understand transaction fees.

PayPal has established itself as a prominent player in the payments industry, offering a straightforward experience for users, especially those new to online transactions. This simplicity translates to minimal coding requirements and eliminates the need for technical jargon.

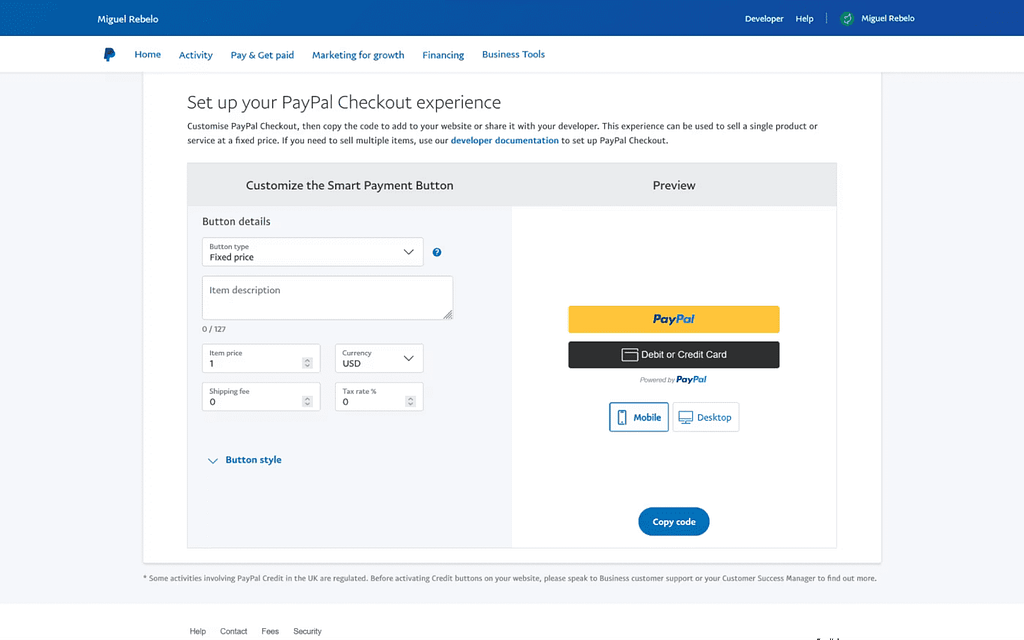

Upon adding products, merchants can customize the Smart Payment Button according to their preferences, with options to adjust the button’s shape, logo, and display of payment methods. After customization, merchants can easily copy the generated code and paste it onto their product pages.

On the customer side, visitors to the website will encounter the configured button, giving them the choice to pay using their PayPal balance or any saved payment method associated with their PayPal account. Alternatively, customers without a PayPal account can opt to enter their credit card details securely. PayPal provides additional security measures such as fraud protection to safeguard against credit card fraud and customer protection to facilitate claims resolution in case of discrepancies between advertised and received products.

However, PayPal’s fee structure is often cited as confusing by users. Transaction fees typically consist of a base fixed price per transaction plus a percentage of the total amount. While the basic credit card fee for U.S. transactions is 3.49% + $0.49, the specific percentage and cents combination vary depending on factors such as transaction type and currency, necessitating careful review of the terms and conditions.

click here – CD ladder: What it is CD ladder and how to build one

Best for mobile payments: Square

Square is a leading player in the mobile payments sector and stands out for its absence of recurring monthly fees for most card processing services. While purchasing a Square register or terminal may entail buying the hardware upfront or paying a monthly fee until the device is fully paid off, card processing services incur only a per-transaction fee.

For card-present transactions, whether conducted in-store or at mobile locations, the cost is 2.6% plus $0.10 per transaction. Online payments, on the other hand, are subject to a fee of 2.9% plus $0.30 per transaction. Keyed-in transactions carry a fee of 3.5% plus $0.15. In the case of invoicing customers through Square, payments related to invoices are charged a fee of 3.3% plus $0.30.

Beyond its mobile and in-person payment offerings, Square provides a range of additional services including payroll, banking, inventory management, restaurant management, and retail inventory solutions, catering to diverse industries.

Pros of Square:

- Seamlessly combines in-person and online sales.

- Includes a basic website builder.

Cons of Square:

- Not as feature-rich as Stripe.

If you’re running a brick-and-mortar shop or not accepting card payments at all, Square can be your solution. It provides full support for physical card reader machines and allows you to create your own online store with seamless payment processing. This means you can boost sales both in person and online.

Square offers a sleek and user-friendly interface. The main dashboard gives you a quick overview of your business, and you can easily access various features through the left-side menu. You can accept payments online for all major card brands, as well as Google Pay, Apple Pay, and Samsung Pay.

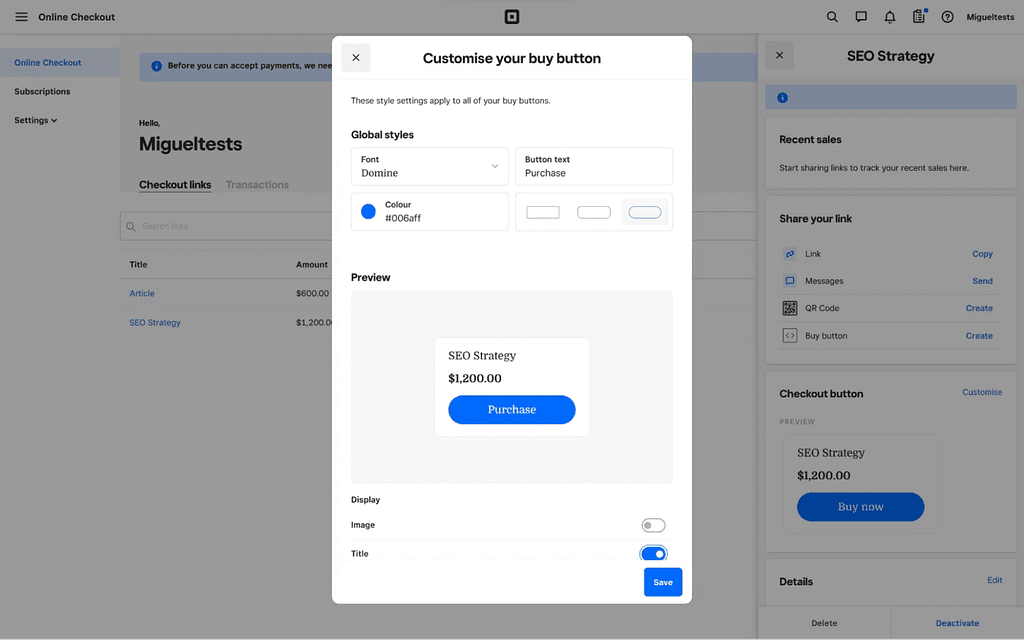

Once you’ve set up your account and added your products, you can embed customizable buy buttons on your sales channels. While the customization options are excellent, it’s worth noting that there are no payment method badges or a “processed securely by Square” note by default. Adding these elements to your website can help reassure your customers that it’s safe to shop with you.

click here – Best 1-Year CD Rates in February 2024

Best for monthly fee only: Payment Depot

If you’re looking to avoid paying a percentage of every transaction, Payment Depot could be the ideal solution. Payment Depot offers a flat monthly fee starting at $79, allowing for unlimited payments up to $250,000 annually. According to Payment Depot, this fee structure can save businesses an average of $400 monthly in payment processing fees.

However, it’s important to note that you’ll still need to cover interchange rates set by Visa and Mastercard, which typically amount to around 2% + $0.10 or $0.22 per transaction.

Payment Depot is compatible with Clover terminals and various other brands. Depending on your processing volumes, Payment Depot may present a favorable option for your business.

Pros:

- Clear and straightforward membership pricing

- Absence of setup fees

- Availability of 24/7 customer support

Cons:

- Limited online support options

- May not be cost-effective for businesses with low transaction volumes

- Not suitable for high-risk merchants

Payment Depot Features

As a simplified payment processing solution, merchants across all Payment Depot plans benefit from the following account features:

- Absence of long-term contracts

- No startup or cancellation fees

- Funds deposited within 24 to 48 hours

- Access to 24/7 customer support via phone, chat, and email

- Online dashboard for monitoring and managing transactions

- Virtual terminal for processing keyed-in payments online

- Integration capabilities with various shopping carts, point-of-sale (POS) systems, and card terminals

- Protection against chargebacks, risk monitoring, and data breach prevention

- No additional charges for statements, PCI compliance, or hidden fees

click here –CD Investments: How Much Can CDs Earn?

Best for monthly subscription pricing: Stax Payments

Stax is renowned as one of the leading credit card processing companies in the US, known for its comprehensive features catering to various business models. One of its standout qualities is its adaptability and suitability for businesses of all types.

Particularly noted for its proficiency in handling high volumes of transactions and sales traffic, Stax excels in effortlessly managing even lower volumes of sales and transactions with ease.

Features Stax Payments

Businesses favor Stax for its array of superlative features tailored to their needs. These features facilitate various business operations, enhancing efficiency and productivity.

- Invoicing:

Simplifying a crucial business process, Stax streamlines invoicing, making it more accessible and professional. With customizable digital invoices, businesses can effortlessly send reminders and track payments across different methods, including cash, credit cards, and checks. - Keyed:

Stax’s Keyed feature enables businesses to accept mobile payments, tapping into the popularity of digital transactions, particularly in retail and e-commerce. By turning mobile devices into Points of Sale (PoS), Stax facilitates seamless online payments, especially via credit cards over the phone, ensuring utmost convenience. - E-commerce:

Tailored for e-commerce businesses, Stax offers dedicated e-commerce features to streamline online transactions. From creating customizable shopping carts to providing instant e-commerce reporting, Stax simplifies the online shopping experience. This feature enables businesses to analyze sales trends and gain valuable insights effortlessly.

Pricing:

- Growth: $99 (Monthly)

- Pro: $159 (Monthly)

- Ultimate: $199 (Monthly)

Pros:

- Mobile-friendly

- Virtual Point of Sale Terminal

- Highly interactive User Interface

- Recommended for high sales volumes

- Low interchange rate

Cons:

- Not suitable for low sales volumes

- Less suitable for small businesses

- Expensive subscription charges

click here – CD Investments: How Much Can CDs Earn?

Best for surcharge compliance: cardX

CardX distinguishes itself as a payment processing platform dedicated to minimizing expenses for merchants. By automatically applying a surcharge to customer transactions, the processor offsets the costs borne by your business. Consequently, credit card processing becomes entirely free on a per-transaction basis, while debit card transactions incur a fee of 2.91%.

With CardX, merchants face a monthly fee, commencing at $29 for online payments and $35 for in-person transactions. Emphasizing compliance, CardX operates in the majority of states nationwide, with some exceptions, notably New York.

Pros:

- Auto surcharging

- Upfront pricing

- Provides signage and merchant training

Cons:

- Card terminals can be expensive

- Lacks accounting integrations

- No card-present point-of-sale integration

CardX Fees

CardX implements a monthly fee, starting at $29 per month, determined by annual sales volume. This fee grants merchants access to both card-present and card-not-present payment processing. With CardX, merchants are relieved of credit card transaction fees due to its surcharging mechanism. However, merchants are still responsible for acceptance fees associated with customers’ debit card usage.

Best for diverse payment methods: Paysafe

Paysafe is a multifaceted payments company encompassing various brands, including the globally recognized peer-to-peer payments app, Skrill. Offering both in-person and online payment solutions, Paysafe caters to a wide range of industries, particularly gaming companies. Through its interchange plus model, merchants pay Paysafe $0.10 and 0.30%, along with applicable interchange fees based on the chosen payment method.

Setting itself apart, Paysafe extends its services beyond traditional card payments. It supports multiple currencies, cryptocurrency transactions, digital wallets, and other payment products. For business owners seeking a comprehensive payment solution capable of handling diverse payment methods, Paysafe presents an attractive option.

Features Paysafe

- Wide industry acceptance: paysafecard enjoys broad acceptance across various sectors, including gaming, e-commerce, and entertainment platforms.

- Secure and private transactions: Customers can make online purchases using paysafecard without divulging personal or financial data, ensuring privacy and security.

- No need for bank accounts or credit cards: paysafecard eliminates the necessity for traditional banking services, making it accessible to individuals without access to such accounts.

- Flexible payment denominations: Customers have the flexibility to select their desired denomination for prepaid vouchers, enabling customized payment options.

- Convenient accessibility: paysafecard vouchers are readily available from authorized retailers or online sources, ensuring convenient access for users.

The Payments API offered by paysafecard addresses the following requirements:

- Payment Instruments: supports paysafecard, paysafecard account, and Scan to Pay.

- Prepaid Payment Method: enables online payments without the need to input personal information or bank/credit card details.

- Transaction types: supports Payments, Withdrawals, and Refunds.

- Payment authentication: ensures PIN protection in compliance with the Payment Services Directive 2 (PSD2).

click here –Are CDs Taxable?

Best for robust payment features: U.S. Bank Merchant Services

If you’re seeking a versatile payment gateway capable of managing both online and in-person transactions, U.S. Bank’s merchant services could be worth exploring. As one of the largest banks in the United States, U.S. Bank offers comprehensive banking and merchant solutions tailored to businesses of all sizes.

For mobile payments, there’s no recurring software fee. Various packages are available for cafes, restaurants, retail outlets, and other brick-and-mortar establishments, ranging from $29 to $99 per month. Additionally, there’s a $29 monthly fee for each additional payment terminal. Each plan offers different features and limits, allowing businesses to select the most suitable option based on their size and industry.

For card-present transactions involving tapping, dipping, or swiping cards, businesses incur a charge of $0.10 per transaction plus 2.6%. Keyed-in transactions for card-not-present scenarios carry a fee of $0.15 plus 3.5%. Online payments are priced at $0.30 per transaction plus 2.9%. With its diverse range of offerings, which cater to both online and offline sales, U.S. Bank’s merchant services are competitively priced and highly effective.

Furthermore, new businesses signing up for U.S. Bank Merchant Services can enjoy an additional benefit. Upon opening a new Platinum Business Money Market account and meeting the specified account criteria, businesses will receive a 2.50% rebate on transaction fees until 2024.

Pros:

- Basic plan has no monthly fee

- Offers same-day funding

- No cancellation fee

- Provides surcharging and debit card optimization programs

Cons:

- Charges a setup fee for higher plans

- Limited user reviews

- Lacks ecommerce integrations

Best for online payments: Stripe

Stripe is an excellent option for businesses that have their own applications or established websites and wish to integrate payment processing seamlessly. Stripe offers developer-friendly payment solutions that easily integrate with various marketplaces and online payment systems using APIs. If you’re using a sales platform optimized for Stripe, connecting your app or website is as easy as copying and pasting a code provided by Stripe.

The standard Stripe online payment processing service comes with a fee of 2.9% plus $0.30 per payment, without any recurring fees. Businesses with high sales volumes may be eligible for discounts through tailored pricing plans.

Stripe pros:

- Highly flexible with a plethora of features

- Extensive ecosystem of plugins and integrations

Stripe cons:

- Slightly more complex setup process

Stripe has become synonymous with online businesses, largely due to its remarkable flexibility and comprehensive toolset. It positions itself as the financial backbone of the internet, and rightfully so.

Upon entering the dashboard, it’s evident that Stripe offers depth, which may initially seem overwhelming. While developers will find it intuitive, beginners might feel daunted. However, Stripe provides an implementation wizard, guiding users through the setup process by asking a series of questions. The results come with a comprehensive guide, simplifying the process of copying and pasting code into the appropriate sections of your website.

Once your store is up and running, Stripe offers extensive insights into your payment activities. You can monitor sales volume, track fraud and disputes, analyze spend per customer, and identify high-risk payments directly from the dashboard. For a deeper analysis, the Reports section provides various options, including billing analytics for examining Monthly Recurring Revenue (MRR) and revenue forecasts.

Another advantage is its straightforward fee structure: 2.9% plus $0.30 per transaction for credit cards, with clear pricing for other payment methods listed on the pricing page.

There are three primary ways to integrate Stripe into your store:

- Embedding an interactive payment form (requires some coding for customization).

- Adding a button that triggers a secure pop-up hosted by Stripe for customers to input their credit card details (also involves coding for implementation).

- Redirecting customers to a visually appealing checkout page where they can enter their details, then returning them to your website upon completion.

Stripe offers a plethora of additional features, catering to users of all expertise levels. Some notable features include subscription management for cross-selling, tax automation, incorporation of startups via Atlas, and seamless integrations with various website builders and eCommerce platforms.

click here –How can I log in to my Discover account online?

Best for single-location businesses: Clover

Clover is a prominent payment processing service directly available to businesses and facilitated through numerous banking partners. With over 3,000 financial institutions, including Citi, PNC, SunTrust, and Wells Fargo, offering Clover, it’s widely accessible.

Ideal for small businesses, such as retailers and restaurants, Clover provides terminals that cater to single-location establishments. However, investing in Clover payment systems entails a significant upfront cost. While some businesses may commence operations without upfront expenses, many others may incur costs ranging from $2,000 to $4,000. Additionally, monthly fees range from $14.95 to $114.85.

Payment charges vary depending on the industry. Typically, businesses pay 2.3% to 2.6% plus $0.10 for card-present transactions and 3.5% plus $0.10 for card-not-present purchases. Depending on the required features, these costs may be justified.

Presently, some businesses may qualify for discounts of up to $1,400 on startup costs, representing substantial savings on card processing hardware.

Best for digital wallet integrations: Braintree

Braintree, a subsidiary of PayPal, is an integrated payment processor that facilitates transactions via credit cards, digital wallets, PayPal, and Venmo. It boasts compatibility with Apple Pay, Google Pay, and all major credit cards, catering to both website and mobile app payments.

For standard mobile wallet and card payments, Braintree charges 2.59% plus $0.49 per transaction. Transactions conducted through Venmo incur a fee of 3.49% + $0.49 per transaction. Additionally, Braintree supports ACH (bank account) payments, imposing a fee of 0.75% up to $5 per transaction. Notably, there are no recurring monthly fees associated with Braintree’s services.

Best for omnichannel payment solutions: Ayden

Adyen is a versatile international payment processor that facilitates transactions across various payment channels, encompassing in-app orders, in-person pickups, self-scan and pay, in-store purchases, home deliveries, QR code payments, and self-service kiosks.

For businesses in the United States, Adyen levies a $0.13 processing fee in addition to an interchange fee determined by the customer’s chosen payment method. Interchange fees typically range between 2% to 4%, though they may vary depending on the specific payment method employed.

Being a global processor, Adyen offers support for a wide array of cards and payment platforms, including Affirm, Alipay, Amazon Pay, Apple Pay, Cash App Pay, Diners Club, Google Pay, JCB, Klarna, Samsung Pay, UnionPay, and WeChat Pay.

click here –How do I make a payment to Synchrony Bank? (2024)

Frequently asked questions (FAQs)

Q.1 How do payment gateways work?

The payment gateway ensures the secure encryption of card details, conducts fraud checks, and then forwards the transaction details to the acquiring bank. Subsequently, the acquiring bank relays this information to the card provider (such as Visa, Mastercard, or Rupay), which, in turn, sends it to the issuing bank for authorization.

Q.2 Can payment gateways accept multiple currencies?

Retailers have the option to set up a payment gateway to accept payments in multiple currencies, allowing customers to choose their preferred currency at checkout. Payment processors typically provide tools for managing exchange rates, allowing merchants to establish an exchange rate markup or margin.

Q.3 Are there any transaction limits with payment gateways?

Debit card transactions in India are subject to regulations set by the Reserve Bank of India (RBI). For ATM withdrawals, the maximum daily limit is capped at Rs. 50,000, while for point-of-sale (POS) transactions, it is set at Rs. 1 lakh per day. These limits are imposed to mitigate unauthorized withdrawals and safeguard the interests of customers.